Token Staking in DeFi: Evaluating Economic Efficiency, Net Effects, and Sustainability

An in-depth analysis of token staking mechanisms in DeFi, exploring economic efficiency, network effects, and long-term sustainability.

Staking is considered as mainstream utility for DeFi tokens, however, in many cases it doesn’t represent the inherit function of network security. In many Web3 projects, staking generates purely inflationary pressure, which is masked as a short-term positive effect due to the locked supply. At Coinstruct, we’ve analyzed staking as tokenomics building-block and provided actionable insights for blockchain founders on how to use the mechanics responsibly.

Economic Benefits and Drawbacks

Staking utility tokens can offer significant economic benefits to DeFi projects. By locking tokens, staking reduces the circulating supply and immediate selling pressure, which can complement price stability and lower volatility. This incentivizes long-term holding: users earn rewards instead of selling, increasing token demand and potentially driving value appreciation over time. Staking programs also foster community engagement and loyalty — participants gain a sense of ownership in the protocol’s success, aligning their incentives with the project. In some cases (e.g. proof-of-stake networks or risk backstop funds), staking enhances network security and reliability, since stakers are financially motivated to act honestly and support the system. These benefits suggest that, when well-designed, staking can be beneficial for a DeFi token economy, promoting stability and user commitment.

However, staking is not that easy– there are drawbacks and sustainability concerns. A major risk is inflationary dilution: if staking rewards come from minting new tokens, the circulating supply grows and each token’s value may drop. Excessive token issuance to pay high APYs can lead to unsustainable “Ponzi-like” dynamics. Indeed, liquidity mining and staking incentives based purely on aggressive emissions have resulted in unsustainable growth: once the yields inevitably diminish, token prices often crash. Another drawback is liquidity trade-off — locking a large portion of supply means fewer tokens in the market, which can reduce sell pressure (good for price) but also make markets thin. Projects have found that when a high percentage of tokens are locked, market liquidity can dry up and price swings become extreme. Aave’s Safety Module addressed this by allowing stakers to also provide liquidity (staking via an AMM pool), ensuring there is still a deep market for the token. Other risks include centralization (large holders dominating staked supply or governance), smart contract vulnerabilities in staking contracts, and regulatory uncertainty if rewards resemble dividends. Overall, while staking can strengthen a DeFi ecosystem by aligning incentives and reducing token velocity, poorly designed programs (e.g. sky-high “yield farms”) may prove unsustainable and harm long-term project health. “50% yield — how is that possible? … This is the definition of a Ponzi scheme”, warning that protocols must ground rewards in real value to be sustainable. In summary, staking’s economic impact cuts both ways: it can stabilize and enrich a token economy, but unchecked inflation or flawed designs pose serious sustainability concerns.

Objective Functions for Staking Optimization

Web3 projects should establish clear objectives for their staking programs, essentially defining what “success” looks like. A common objective is maximizing the stake participation rate (the percentage of token supply staked) without compromising other goals like liquidity or user growth. For example, Synthetix introduced inflation in 2019 specifically to boost its staking rate, which reached an industry-leading ~70–80% of supply. Over time, Synthetix even adjusted rewards dynamically to target a desired staking ratio (The End of Synthetix Token Inflation). Many networks take a similar approach: Polkadot’s design targets roughly 50% of DOT staked, using a 10% annual inflation that is “meant to help strike a balance between the users who stake and the users who participate in parachain auctions.” In Polkadot’s system, if only 50% of tokens are staked, those stakers receive all the inflation (effectively ~20% APY), whereas if a higher percentage stakes, the reward per staker is lower (Why is Polkadot having the highest staking percentage in crypto? : r/Polkadot). This reflects an optimization goal: ensure staking is sufficiently attractive to secure the network while not outpacing other token utilities.

Beyond stake ratio, projects define success via multiple metrics. These can include the security threshold (enough value staked to secure the protocol or cover risks), user adoption (number of unique stakers, indicating decentralization of ownership), and retention/lock-up duration (longer average staking periods signal long-term confidence). There is an inherent trade-off akin to a “staking trilemma” among security, user growth, and token appreciation. If a project prioritizes security with strict staking requirements (high minimum lockup or slashing penalties), it may deter participation and reduce the total staked percentage. Conversely, making staking too easy (no lockup, no risk) can maximize participation but might not filter for reliable validators or loyal holders. Thus, optimizing staking requires balancing these factors according to the project’s stage and needs.

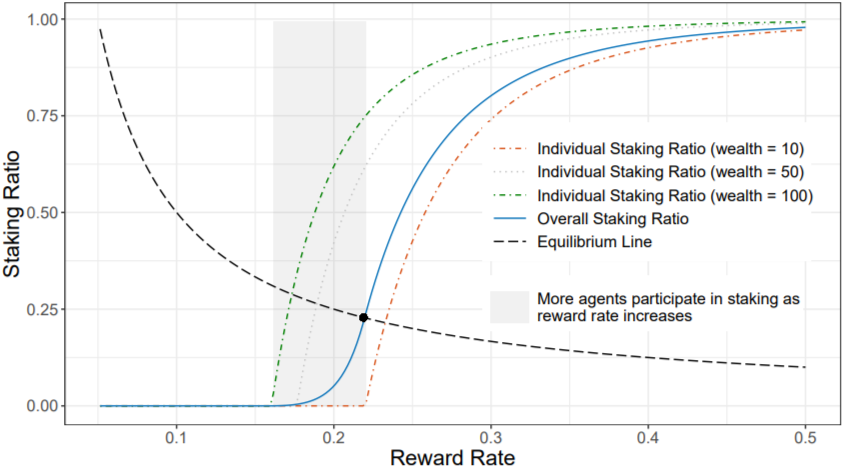

Individual staking decisions and equilibrium staking ratio

In practice, key parameters are tuned to achieve the chosen objectives. Projects set reward rates to be competitive enough to entice staking but not so high as to cause runaway inflation. Data shows a clear correlation: higher reward rates do draw higher staking participation. For instance, one study found that a 1% increase in a token’s staking APR leads to a measurable uptick in staking ratio the following week. However, the model also implies diminishing returns — as more tokens get staked, the reward per token typically drops (since a fixed pool is shared more widely). This means protocols often have an implicit optimization function like “maximize staking ratio subject to a sustainable inflation rate”. Some use algorithmic adjustments: Polkadot and others explicitly adjust payouts based on current staking levels (to hit a target ratio), while Cardano chose a modest ~5% reward rate aiming for broad participation without high inflation. Another success metric is protocol value generated per token emitted — essentially, are staking rewards earning their keep? An optimal program should result in value-added behaviors (security, fee generation, user growth) that justify the cost. A weakness in some staking designs is the lack of equivalency between rewards paid out to users and value generated for the protocol as a result of staking. In other words, projects seek to align staking incentives with productive outcomes. If staking merely locks tokens but doesn’t benefit the protocol (no security contribution, no fees generated), then high rewards are just a costly marketing device. Successful Web3 teams define objective functions that maximize genuine network benefits (security, usage, loyalty) per unit of reward issued, thereby optimizing staking for long-term value rather than short-term hype.

Net Effects of Staking on Project Sustainability

The net impact of staking on a project’s sustainability can be double-edged. On one hand, staking tends to increase token demand and reduce supply in circulation, which can support the token’s price stability. Empirical evidence shows that when more tokens are staked (i.e. removed from liquid supply), it often correlates with positive price appreciation. This makes intuitive sense: staking slows token velocity, as holders keep tokens locked for rewards instead of trading them, which creates a kind of “convenience yield” for holding the token. In the short to medium term, this can boost valuation because fewer tokens are being sold and more investors are attracted by the yield. A vibrant staking program can thus foster a virtuous cycle: high participation -> lower float -> upward price pressure -> more demand to stake. Many DeFi projects benefited from this dynamic during growth phases, effectively using staking to bootstrap network effects and liquidity. Synthetix, for example, credited its inflationary staking rewards with creating a “bull market in liquidity and protocol growth” during its early expansion (The End of Synthetix Token Inflation). Additionally, staking can contribute to price resiliency. Even during market downturns, holders who are earning staking income may be less inclined to sell, providing a stabilizing effect. In these ways, staking can be a net positive for a project’s sustainability, if it leads to a loyal user base and a controlled token economy.

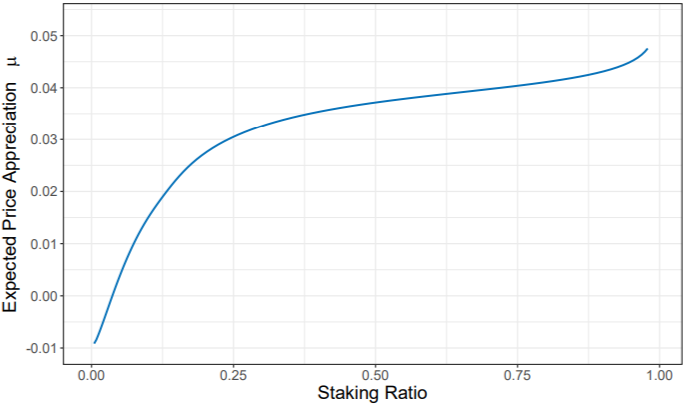

Staking ratio and price dynamics

This graph above shows the relationship between the system staking ratio and the drift term of the token price (µ). As this graph shows, greater staking ratio relates to higher expected price appreciation. Specifically, µ exhibits a roughly convex increase in (0, 1) with an additional lift when staking ratio is sufficiently high.

On the other hand, poorly calibrated staking can undermine sustainability. The most obvious issue is inflation. If a protocol continuously mints new tokens for stakers without equivalent growth in real demand, the token’s value will erode over time. “Rewarding users with new tokens can increase the circulating supply, potentially reducing token value through inflation,” as one risk assessment notes (EEA DeFi Risk Assessment Guidelines version-after-1 — Editor’s Working Draft). Many DeFi projects learned this the hard way: excessive token emissions to fuel staking or yield farming led to short-lived price pumps followed by sharp collapses once selling pressure caught up. A notorious example was the collapse of Terra’s ecosystem in 2022 — its Anchor protocol offered 20% APY on stablecoins, a rate maintained by drawing down reserves. This attracted huge deposits (like a staking demand for UST), but proved completely unsustainable; when the reserves emptied, confidence vanished and the entire token system (UST and LUNA) imploded, wiping out billions. While Anchor’s case is not a typical utility token stake, it exemplifies how outsized “risk-free” yields breed fragility. Even less dramatic cases saw “unsustainable growth” from liquidity mining incentives, only to crash when rewards dried up. Projects that deplete their treasuries or endlessly mint tokens to pay stakers are effectively borrowing against future value — if that future value doesn’t materialize (via greater adoption or revenue), the scheme collapses. Thus, a crucial aspect of sustainability is funding staking rewards from real economic value (fees or profits) rather than solely printing tokens. The recent “real yield” movement in DeFi reflects this, emphasizing that protocols should aim to reward stakers out of actual revenue streams, not just inflation.

Another net effect to consider is on liquidity and token velocity. Moderate reductions in token velocity (through staking locks) can be beneficial, but extreme reductions can make the token less usable and markets less liquid. If 90% of a token’s supply is locked up, the remaining 10% in circulation might trade in a very thin market — ironically, that can increase volatility, as even small sell orders move the price. Aave’s team explicitly noted this issue: tokens with traditional lockup staking schemes “tend to suffer from low market liquidity and extreme volatility when high percentages of the total supply are being locked.”. By allowing part of their staking to occur via liquidity pool tokens, Aave ensured that a chunk of AAVE remained available in the market, alleviating this problem. This illustrates that healthy liquidity must be maintained for a token even while encouraging staking; otherwise the project could face wild price swings or inability for new users to acquire tokens to participate. Additionally, extremely low token velocity might indicate that the token isn’t finding use in the ecosystem (beyond pure staking), which can be a red flag. Sustainable projects balance staking with other token utilities (trading, spending for fees, governance, etc.) to keep the economy active.

In summary, the net effects of staking on sustainability depend on balance. Staking often reduces sell pressure and can enhance price stability and demand, which is positive for longevity. It also aligns users to think long-term, arguably strengthening community and governance (stakers are incented to care about the protocol’s health). However, if those rewards are funded by unsustainable inflation, the apparent stability can be false and temporary. A project might enjoy a period of price support as tokens are locked up, only to face a “Day of Reckoning” when large unlocks occur or when reward emissions are cut. The key is ensuring that staking is part of a holistic tokenomic design: ideally, rewards either taper down as natural demand grows, or shift to being funded by actual protocol revenue. For example, Synthetix, after years of inflationary rewards, recently ended SNX inflation and transitioned to using protocol trading fees to reward holders (via buy-and-burn) — a move towards long-term sustainability (The End of Synthetix Token Inflation). Likewise, PancakeSwap moved from high-emission CAKE rewards to a model of net deflation (burning more tokens than issued) once it achieved sufficient adoption. These adjustments show that staking can be sustainable if treated as a phase in growth and later replaced or supplemented with “real yield” mechanisms. In conclusion, staking’s net effect can enhance project sustainability when properly managed, but if mismanaged, it can undermine a project by inflating away value or choking token liquidity. Successful protocols continually tweak their staking parameters to align with actual usage and to avoid the pitfalls of unchecked inflation.

Types of Staking Rewards

Staking reward systems in DeFi come in various structures, each with different implications for participants and the project. Broadly, we can categorize staking reward models by how the rewards are determined and how they are funded:

Fixed vs. Dynamic Rewards: Some projects offer a fixed reward rate or amount, whereas others have dynamic payouts. In a fixed APR model, stakers might earn a flat X% annually regardless of how many others are staking. This often requires the protocol to mint whatever amount of tokens needed to meet that rate (which can lead to unpredictable inflation if participation changes). By contrast, many protocols use a dynamic pool of rewards — e.g. a fixed number of tokens per block split among all stakers. In such cases, the individual yield (APY) varies: if more people stake, each person gets a smaller slice (diluting the yield), and if few stake, the yield is higher. For example, Polkadot fixes its inflation at ~10% of total supply, allocated to stakers and the treasury. If 50% of DOT is staked, those stakers collectively receive ~5% of the supply (the other ~5% goes to treasury), which means each staker effectively gets 10% yield on their stake (since they’re among the 50% receiving 5% of supply) (Why is Polkadot having the highest staking percentage in crypto? : r/Polkadot). If 100% of DOT were staked, each would only get 10%. This is a dynamic reward distribution by design — user staking rewards change based on participation, even though total inflation is fixed. Other networks like Cosmos follow a similar approach, targeting a staking ratio and adjusting the reward rate if the actual ratio deviates (this ensures neither under- nor over-incentivization of staking). In summary, fixed-rate models give certainty to stakers but can cause runaway token issuance if not capped, while dynamic-rate models naturally adjust incentive strength and often are more sustainable long term.

Inflationary vs. Non-Inflationary Funding: Staking rewards must come from somewhere — either new token issuance (inflation) or existing value/revenue. The prevalent model in many PoS chains and DeFi protocols has been inflationary rewards: minting new tokens on a schedule to pay stakers. This adds to the token’s supply (hence the inflation risk discussed earlier). Examples: Cosmos (ATOM) has a variable inflation rate (up to ~20%) to maintain a target stake rate, Polkadot (DOT) uses a fixed 10% inflation, and Synthetix (SNX) had a declining inflation schedule that started very high (~75% APY) and tapered down to single digits before being turned off. Inflation-funded rewards are easy to implement and guarantee that stakers earn tokens, but they dilute existing holders. On the other hand, some projects aim for non-inflationary rewards — meaning the token supply doesn’t increase to pay stakers. Instead, rewards are paid from real yield or reserves: for instance, fee revenue sharing, treasury funds, or other tokens. A notable trend is revenue-sharing models: protocols like SushiSwap, GMX, or dYdX distribute a portion of the protocol’s fees to those who stake or lock the governance token. In the case of GMX, 30% of all trading fees on the platform are paid out to GMX stakers (in ETH), rather than issuing new GMX. This means the reward is sourced from actual usage of the platform (and is thus sometimes called “real yield”. Similarly, SushiSwap’s xSUSHI model gave stakers a share of DEX trading fees, and MakerDAO has discussed paying MKR holders from stability fees. The benefit of revenue-based rewards is sustainability — they scale with the protocol’s success and don’t inflate the token supply. A drawback is that if usage is low, the rewards can be meager (so there’s less short-term allure compared to high inflation APYs). Some projects initially use inflation to bootstrap staking but later transition to fee-based rewards (as Synthetix did by ending SNX inflation and planning fee-based buybacks. It’s worth noting a hybrid approach too: a project might allocate a fixed budget from its token treasury for staking incentives (effectively pre-mined rewards). For example, a DAO could decide that 10% of total token supply (from its reserves) will be gradually paid out as staking rewards over 3 years. This isn’t inflation if those tokens were already counted in supply, but it is a form of distribution. The sustainability then hinges on what happens after that allocation is exhausted — ideally by then the network generates enough fees or value to continue rewarding long-term holders in other ways.

Tiered and Duration-Based Rewards: Many DeFi staking schemes incorporate tiers or locking periods to encourage certain behaviors. In tiered staking models, users might receive different benefits based on how much they stake or hold. For instance, some exchange tokens (like those of Binance or Crypto.com) offer tiered perks: holding more tokens (often “staking” them in a wallet) can grant higher cashback, trading fee discounts, or access to special opportunities. While not a direct APY, these are staking-like utilities where token lockup confers privileges. From the protocol perspective, the objective is to incentivize larger or more committed holders. Duration-based rewards reward users for locking tokens for longer periods. A common design is to offer a yield bonus for longer lockups: e.g. lock for 1 month vs 1 year vs 4 years and get progressively higher APY or a multiplier on rewards. This was exemplified in the Curve Finance “veCRV” model — users lock CRV tokens for up to 4 years to get voting power and fee boosts, with longer locks giving proportionally more power. Another example is the Aethir project’s staking: a 4-year lock earned an estimated 261% APR vs ~195% for 3-year, down too much lower for short locks. In their system, someone staking a small amount for a long duration could equal the rewards of someone staking a much larger amount for a short time, strongly encouraging long-term commitment. The idea behind duration incentives is to maximize retention — if users lock their tokens for extended periods, it signals trust in the project’s future and reduces likelihood of sudden sell-offs. Tiered models can also be combined with duration: e.g. a platinum tier if you stake over 10,000 tokens for at least 1 year, etc. The drawback of requiring long locks is it reduces flexibility for users and, as noted, can reduce liquidity. So some protocols find a middle ground, offering moderate boosts for longer locks but not punishing those who prefer flexibility.

Case Studies: Successes and Failures

Successful Implementations: A number of DeFi projects have launched staking programs that achieved their intended goals and provided valuable lessons. One prominent case is Synthetix (SNX). In 2019, after pivoting from the Havven project, Synthetix introduced aggressive inflationary staking rewards to encourage people to stake SNX and collateralize the synthetic assets on the platform. This was highly successful in the early years — SNX staking reached very high levels (most SNX in circulation became locked as collateral), which helped ensure liquidity for synth trades and align the community. The inflation schedule was front-loaded (starting very high and decreasing weekly), creating a “bull market in liquidity and protocol growth” as described by the team. Over time, as Synthetix gained real usage (generating trading fee revenue) and as the inflation rate dropped, the impact of inflationary rewards waned. By 2023, SNX inflation had fallen to single digits and was no longer a powerful incentive. Synthetix’s community governance voted to end inflation entirely in late 2023 (SIP-2043), marking a pivot to a new model where staking yields come from actual protocol fees and possibly token buybacks. This case demonstrates a successful use of staking in bootstrapping network effects: inflation was used as a temporary tool to achieve critical mass, and once the protocol matured, they transitioned away from dilution. The key lesson is the importance of an exit strategy from inflation — Synthetix recognized when inflation became “less effective as an incentive” and decisively moved to a more sustainable approach. The project has remained one of DeFi’s staples, suggesting that this calibrated approach (high early rewards, gradually reduced) can work if managed well.

Another success is Aave’s Safety Module. Aave is a lending protocol whose staking mechanism wasn’t about earning massive APY, but about risk management. AAVE token holders can stake into the Safety Module to act as an insurance pool for the protocol (up to 30% of staked AAVE can be slashed to cover shortfall events). In return, stakers earn Safety Incentives (paid in AAVE). This design achieved multiple goals: it gave the AAVE token a purpose beyond governance, increased holders’ commitment (since by staking they accept risk of loss if the protocol fails), and dramatically boosted confidence in the Aave platform (users know there is a sizable economic backstop). The staking participation in Aave’s Safety Module has been strong, and notably Aave tackled the liquidity issue by allowing half of the Safety Module to consist of AAVE/ETH liquidity provider tokens. This way, even staked AAVE contributed to available market liquidity. Aave’s staking yields have been relatively moderate (often single-digit percentages), and there haven’t been major shortfall events requiring slashing — meaning the Safety Module acted as a preventative security measure. The success here is in showing that staking can be used for more than just emissions — it can reinforce a protocol’s robustness. It’s a model of sustainable incentives: the reward rate is calibrated such that Aave’s token inflation is low (AAVE has a fixed supply, so incentives come from an ecosystem reserve), and the benefit to the protocol (insurance) clearly outweighs the cost. The takeaway is that aligning staking with a core utility (insurance/security in this case) creates a win-win for token holders and protocol users.

We also see success in projects embracing “real yield” staking. GMX, a decentralized perpetual exchange, launched in 2021 and gained traction by offering a staking model where GMX token stakers earn a share of protocol revenues (30% of trading fees, paid in ETH). Although the percentage yield to GMX stakers might appear modest (often a single-digit % in ETH), the market rewarded this model: during a bear market, GMX’s token price performed exceptionally well, as investors valued the genuine cash flows to stakers. GMX demonstrated that even a relatively low APY can attract sticky holders if it’s perceived as reliable and tied to real usage. Its success has been cited as evidence that DeFi projects can thrive without outsized inflation — “real yield” from fees created deep liquidity and community confidence. Similarly, older examples like MakerDAO (while it doesn’t have staking per se) showed the power of token burn/value accrual: Maker used to burn MKR from fees, indirectly rewarding holders via deflation, which helped MKR maintain value. Curve’s veCRV mechanism is another success worth noting: by locking CRV for long durations to get veCRV, users gained fee rewards and voting power. This led to over 50% of CRV supply being locked for up to 4 years, massively reducing sell pressure and creating a competitive moat (the so-called “Curve Wars” where other protocols sought veCRV to boost yields). The result was a relatively resilient token economy where the token’s value was intertwined with governance influence and platform fees — a more complex but effective staking/locking strategy that sustained Curve’s dominance in stablecoin liquidity.

Failures and Cautionary Tales: For every success, there are staking implementations that failed or backfired. A prominent failure was the spate of high-APY “DeFi farm” tokens in 2020–21. During DeFi Summer, countless projects offered four or five-digit annualized yields for staking or liquidity farming their tokens. These included meme-themed experiments (YAM, HOTDOG, etc.) and forks of projects like SushiSwap. While a few projects like SushiSwap itself managed to pivot to a more stable model, many of these farms collapsed under sell pressure. The pattern was usually: enormous APY attracts inflows, token price shoots up briefly, then as soon as the market senses the yield is unsustainable (or rewards are dumped en masse by farmers), the price craters. Investors treated these like Ponzi schemes, jumping in early and trying to exit before the inevitable crash. As Cointelegraph Magazine recounted, “Liquidity mining resulted in unsustainable growth, and when yields diminished, token prices dropped. Depleting DAO treasuries to supply rewards programs — or simply minting more and more tokens — for new joiners looked like a Ponzi scheme”. Many sophisticated players even admitted they “paid for their lifestyle by staking tokens [in 2020–21] — even knowing it was akin to a Ponzi scheme about to collapse.” . The clear lesson is that extreme inflation and pure token-incentive feedback loops are not sustainable. They can temporarily boost metrics (TVL, price, etc.), but they do so by borrowing future value. Eventually the music stops, as seen with numerous failed yield farms.

Another cautionary case is Terra’s Anchor Protocol, as mentioned, which offered 20% yield on UST stablecoin “staking”. For a while, this attracted tens of billions in deposits (UST demand), propping up UST’s value and by extension LUNA’s price. But since the yield far exceeded organic earnings (loan interest), it was subsidized by the Terra treasury — essentially a giant bounty to attract users. This worked until the treasury ran low and sentiment turned, leading to a run on withdrawals and the collapse of UST’s peg. The Terra case is extreme, but it underscores a general point: if staking yields are divorced from real economic activity, the system’s stability is in peril. It’s a failure of aligning incentives with sustainability.

We also have examples of governance tokens that stagnated due to lack of staking utility. For instance, Uniswap’s UNI token launched as pure governance with no staking or fee dividend. Initial excitement pushed UNI’s market cap high, but over time some questioned its value since UNI holders had no share of Uniswap’s massive trading fees. The token’s price stagnated relative to peers that did offer staking rewards or fee capture. This isn’t a failure in the catastrophic sense, but it shows that not leveraging staking/utility can be an opportunity cost. (Uniswap governance has since considered fee switch mechanisms to give UNI holders revenue — a recognition that some form of reward may be needed to satisfy holders.)

Finally, consider projects with complicated or overly restrictive staking that saw low uptake. A hypothetical example: if a new protocol requires a 1-year minimum lockup to stake for just a 5% reward, few might participate because the risk and illiquidity outweigh the reward. This could be viewed as a failure of design — misjudging user preferences. In contrast, flexible or liquid staking options (where users can still trade their staked positions, like Lido’s stETH for Ethereum) have generally seen higher adoption. So, a lesson is that usability matters: staking that is too complex or onerous can fail to gain traction, and then the token doesn’t reap any of the intended benefits.

Key Lessons: Successful staking implementations tend to match rewards to actual value creation, either initially or eventually. They also often incorporate flexibility and long-term vision. Synthetix showed the importance of adjusting tokenomics as conditions change (inflation was a kickstarter, not a permanent crutch). Aave demonstrated tying staking to a clear utility (safety) can yield durable benefits. Newer projects like GMX illustrate that lower, sustainable yields can beat higher, unsustainable ones in the eyes of investors who think long term. On the flip side, the failures teach us that yield hype is transient — without sustainable economics, staking can hasten a project’s downfall by attracting mercenaries rather than true supporters. Projects that drained their treasuries or over-inflated their supply to fuel short-term demand ultimately damaged their credibility and token value. The overall takeaway is that staking is a powerful tool — like a lever that can amplify either sound or unsound economics. The successes came from treating staking as part of a broader strategy (security, growth, revenue sharing), whereas the failures treated staking rewards as an end in themselves (just to pump metrics). Future DeFi projects are increasingly designing staking with these lessons in mind, aiming to replicate the successes and avoid the pitfalls.

Comparison with Alternative Token Utility Mechanisms

Staking is just one way to endow a utility token with value and utility. It’s instructive to compare staking with other common token utility mechanisms such as governance rights, yield farming incentives, and fee-sharing models (dividends or buybacks). Each mechanism has its role, and many projects combine several to create a well-rounded token economy. Here, we analyze how staking stacks up against these alternatives:

Staking vs. Governance-Only Tokens: Governance tokens give holders voting power over protocol decisions (e.g. MakerDAO’s MKR or Uniswap’s UNI). By itself, governance can be valuable — it lets token holders influence fees, upgrades, and treasury usage, which in theory should be reflected in token price if holders expect to steer the protocol toward growth. However, governance is a non-financial utility; it doesn’t directly reward holders except through the indirect impact of good governance on token value. Staking, on the other hand, typically provides a direct financial incentive (yield) for holding the token. In practice, tokens that are governance-only often face demand limitations: many investors are not interested in active governance and would prefer a tangible return. For example, UNI had a huge distribution but relatively low voter turnout — most holders treated it as an investment rather than a vote. Staking can complement governance by giving passive holders a reason to stick around (earn yield) and participate at least by locking up their tokens. Some projects explicitly tie governance to staking: for instance, Curve’s vote-escrow model requires locking tokens to gain voting weight, effectively merging staking and governance (you commit long-term to have a say). This can strengthen governance by ensuring only long-term aligned holders influence the protocol. In summary, compared to pure governance tokens, staking adds an extra layer of incentive. It can be seen as a way of distributing “dividends” to token holders (if rewards come from fees or inflation), whereas governance alone doesn’t do that. That said, governance utility is crucial for decentralization — staking yields mean little if the protocol isn’t well-run. The two are not mutually exclusive; indeed, many tokens serve both purposes (you stake the token to earn rewards and you get voting rights while staked). A key difference is in audience: governance appeals to users who want voice in the system, while staking appeals to those who want an economic reason to hold the token. A robust token often needs both: fundamental control rights and financial incentives.

Staking vs. Yield Farming (Liquidity Mining): Yield farming usually refers to providing some service (often liquidity provision) in exchange for token rewards. It rose to prominence with Compound’s COMP distribution and the wave of liquidity mining programs in DeFi Summer 2020. The difference from basic staking is that yield farmers must typically do more than hold the token — they might have to supply liquidity to a pool, lend assets, or stake LP tokens rather than the governance token itself. In effect, yield farming is a customer/user acquisition strategy: you reward users (with your token) for performing actions that benefit the protocol (like seeding liquidity or usage). Staking, in contrast, often just requires holding the token and locking it. So, how do they compare? Yield farming tends to offer higher potential returns but with higher effort and risk. Farmers often chase the best APYs across platforms, leading to a lot of short-term, “mercurial” capital. Staking usually provides a more stable and predictable return, appealing to long-term holders who want to support the project rather than chase every last percent. Yield farming can rapidly bootstrap liquidity (e.g. a new DEX token incentivizing LPs can achieve high TVL in weeks), but it can also cause huge sell-pressure as farmers dump the reward tokens continuously (many early DeFi projects experienced this). Staking, by locking tokens, usually reduces sell pressure rather than increasing it. So, one might say yield farming is a growth hack — great for kickstarting network effects — whereas staking is more of a retention and alignment mechanism. They target different behaviors: yield farming says “use our product and we’ll give you tokens,” staking says “hold our token and we’ll reward you for loyalty.” In practice, projects use both: e.g. a DEX might distribute tokens to LPs (yield farming) to ensure liquidity, and also allow those tokens to be staked for additional rewards or fee share (staking) to encourage keeping them. The risk profile differs too — yield farming often involves smart contract risk and, if providing liquidity, impermanent loss, etc. Staking is generally simpler (though smart contract risk still exists). For new/inexperienced users, staking is usually seen as lower risk and easier, while yield farming is for those willing to actively manage positions for higher returns. To sum up, yield farming complements staking: use farming to distribute tokens widely and build utility (liquidity, lending volume), then use staking to give those token holders a reason to stay invested. Without staking or some value accrual, yield-farmed tokens can suffer the fate of being mercilessly dumped once farming ends (as we saw with many liquidity mining schemes). So, staking can be the bridge that converts transient yield farmers into long-term stakeholders by offering ongoing rewards or rights after the initial farming phase.

Staking vs. Fee-Sharing / Dividend Models: Fee-sharing refers to mechanisms where token holders receive a portion of the revenues or fees that the protocol generates. This can be implemented by direct distribution (e.g. buy-and-distribute or a treasury that pays out) or indirectly through buybacks and burns that increase each holder’s share of the pie. Fee-sharing is often considered a form of staking reward — typically, users must stake or lock the token to claim their fee share (to avoid just anyone holding temporarily through the snapshot date). The recent focus on “real yield” in DeFi is essentially highlighting fee-sharing models: “Real yield is a DeFi metric where stakers’ earnings come from the protocol’s revenue, such as fees, instead of aggressive token emissions.” . The advantage of fee-sharing is that it links token value to platform success: if volume and fees go up, stakers earn more, theoretically making the token more valuable (like a stock with higher dividends). As one analysis puts it, an increase in a token’s cash flow will directly increase its fundamental value, “which in turn increases demand until supply and demand reach a balance” . However, many first-generation governance tokens did not include fee-sharing, which led to situations where tokens didn’t reflect the protocol’s high usage. For example, Uniswap, as mentioned, charges trading fees but those fees all went to liquidity providers; UNI holders got none of it, so UNI’s value was based on speculation of future fee-sharing or just governance sentiment. Staking shines in fee-sharing models: usually, to implement revenue sharing, projects ask users to stake the token to start earning their share (this prevents a scenario where someone could buy the token for a minute, claim fees, and sell). For instance, SushiSwap’s xSUSHI required users to stake SUSHI in an xSUSHI contract, which would accumulate 0.05% of all swap fees in the form of more SUSHI (bought from the market). The xSUSHI stake represented your share in that fee pool. This is both staking and fee-sharing combined. Another example, GMX as discussed, shares fees directly to stakers in ETH, aligning token rewards with actual platform usage. The trade-off here is regulatory and conceptual: a pure fee/dividend token starts to resemble a security (since it provides passive income from others’ efforts). Some projects avoid explicit fee dividends for this reason, opting for buyback-and-burn (which still benefits holders but indirectly). But from a token holder’s perspective, fee-sharing is highly attractive — it means the token is a productive asset not just a governance chip. Relative to a pure staking model with inflation, fee-sharing tends to yield lower APYs initially but those APYs are sustainable. For instance, a young project might be able to offer 100% APY by printing tokens, but a mature fee-based token might only yield 5% from fees; nonetheless, the latter can carry a higher valuation because investors can model it like a cash flow. We saw this with exchange tokens (e.g. Binance’s BNB uses a combination of quarterly burns (from exchange profits) and other utilities. Those models helped establish expectations of value. It’s important to note that staking is often the vehicle for fee-sharing — you usually have to stake to get the fees. So in comparing staking vs fee-sharing, it’s not either-or: staking is the mechanism, fee-sharing is the source of rewards. A fair comparison is inflationary staking vs fee-sharing staking. The clear trend is that the market favors fee-funded staking rewards over pure inflation. Projects that pivot to revenue share (like Synthetix planning to use trading fees for SNX buybacks are trying to move into that sustainable quadrant. In concept, fee-sharing gives a token intrinsic value (cash flows), whereas inflationary staking merely redistributes value among holders (some win by staking, others lose by dilution). One caveat: fee-sharing requires the protocol to be actually profitable; in early stages, not all are, so they might rely on inflation as a bootstrap before fees matter.

In comparing all these mechanisms, it’s clear they serve different purposes and can coexist. Many top projects use a mix: Governance to decentralize control, staking (with some inflation early on and fee share later) to reward and retain participants, and yield farming to jump-start usage where needed (like liquidity). For example, Compound had no native staking, but they yield-farmed COMP out to borrowers and lenders to capture market share in lending — massively successful in the short term but eventually the market saturated and COMP’s price declined as emissions continued without new growth. In hindsight, Compound might have benefited from a staking mechanism to lock COMP or distribute protocol interest to COMP holders (some later protocols like Venus on BSC did this by funneling some borrower interest to token stakers). Meanwhile, Curve took a very different path by tying token utility primarily to governance and staking (veCRV) and minimal liquidity mining beyond that — and it has kept value relatively better. Balancer and others combine liquidity mining (for bootstrapping pools) with vote-escrow staking (for governance and fee share).

To encapsulate the comparison: Staking vs other utilities is often a question of immediate tangible rewards vs. long-term or intangible benefits. Governance is intangible but vital; yield farming is immediate but temporary; fee-sharing via staking is tangible and (ideally) perpetual. Staking tends to increase token demand directly (who doesn’t want to earn extra tokens or fees?), while pure governance might not attract as broad a base until the project is very influential. Yield farming can temporarily spike token velocity (farmers get tokens and often sell them quickly), whereas staking reduces velocity (holders lock up for yield). Thus, staking usually contributes more to price stability than yield farming, which can do the opposite if not carefully managed.

In practice, token designs are evolving to incorporate the best of all worlds: for instance, newer governance tokens often include fee-sharing from day one, and also allow staking to boost governance power or yield (so holders have multiple reasons not to sell). We also see more creative mechanisms like bonding (OlympusDAO) or locking with boosts (Solidly, Aura), which are variations on staking to enhance utility or direct rewards. Those go beyond the scope of this analysis, but they reflect the trend of blending utility mechanisms. The bottom line is that staking remains one of the most practical and straightforward ways to reward token holders, and when combined with other utilities, it can significantly strengthen a token’s value proposition. A token that only has one utility (be it just governance, or just fee share, or just staking with no real revenue) is at a disadvantage compared to tokens that manage to be multi-functional. For example, BNB has utility for fee discounts, network gas, launchpad access, and can be staked/validated on BSC — a multifaceted approach that has helped it maintain strong demand.

In conclusion

Staking compared to other mechanisms offers a more predictable, loyalty-based incentive as opposed to the action-based incentive of yield farming or the speculative value of pure governance. Fee-sharing models often use staking as the distribution method, so staking is integral to realizing that utility. Rather than viewing these mechanisms in isolation, projects design a tokenomics mix that fits their goals: staking to solidify a holder base and align incentives, governance to decentralize control, yield farming to grow usage, and fee-sharing or burns to give fundamental value. The art of token economic design is in balancing these elements without introducing contradictions. When done well, staking complements the other token utilities and drives a clearer, more compelling value narrative: “Hold and stake our token for voice in the system, a share of the revenue, and a yield on your assets,” which is certainly more attractive than “Hold our token because… well, just trust us it might be worth something.” As the DeFi sector matures, we see less reliance on hype and more on practical utility — staking is most effective when it’s part of that practical utility set, not just a gimmick. It remains a cornerstone of token design in Web3, but it works best in concert with the other mechanisms that together make a token truly useful and valuable.

Coinstruct — is a specialized agency for full-cycle Web3 tokenomics development where we have a team of diverse specialists from PhD mathematicians, computer scientists to degens from leading DAOs working together to create advanced token models, reward systems, economy audits and scoring. Our focus is to create Web3-native sustainable economic solutions to help crypto projects achieve desired goals through tokens: from fundraising to increasing user base, retention and loyalty. We have successfully developed more than 40 blockchain-based economies for various Web3 ventures (DEXes, CEXes, GameFi, FinTech, DEXes, OTC platforms, P2E, NFTs and many more).

Contact Coinstruct today — to create tokenomics that work.